CPI Report Impact on Construction Outlook

- Ed Sullivan

- Jul 15, 2025

- 2 min read

Updated: Oct 18, 2025

Today’s CPI Report Impact on Construction Outlook

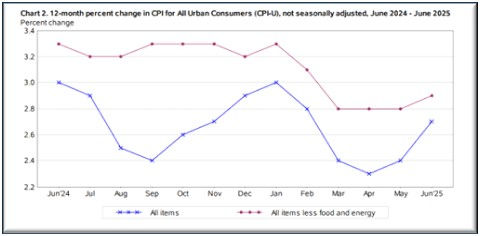

The Data: The Bureau of Labor Statistics (BLS) Consumer Inflation Report released today (July 2025) showed a modest increase in the inflation rate – the first increase since January. The annualized rate now stands at 2.7%, compared to 2.8% recorded since March. The core rate (excluding food and energy price changes) rose for the second consecutive month.

Data Insight: The marginal increase will likely prompt Administration officials to suggest the tariff impact on inflation is overstated. Antagonists to the Administration will suggest that the small uptick in the inflation rate is a sign of more aggressive inflation that lies ahead.

To be fair, the initial tariff impacts will take time for their impact to be realized in data – perhaps not until early fall. Keep in mind, tariff policy is a moving target. New tariffs have been imposed or threaten to be imposed on a regular basis. If enacted, these tariffs threaten even further inflationary threats in subsequent months/quarters.

Policy Impact: The latest data adds little insight regarding the direction of future inflation. This is likely the way the Federal Reserve will read the new data release. If so, it means the Fed will remain comfortable in sitting - opting not to cut rates at the next FOMC meeting at the end of July.

Construction Impact: The construction activity will not improve without a reduction in interest rates. The latest data suggests high-inflation premiums and restrained monetary policy will remain in place beyond the July 2025 meeting. Even if rate cuts materialize at the September 2025 Federal Open Market Committee (FOMC) meeting, given lags, the impacts probably won’t materialize until after the peak construction season (April thru August) has passed. If so, real private construction will take a step back in 2025.

Next Year’s Planning Guidance: Tariff policy adds to the probability of inflation. I expect inflation will become evident in the fourth quarter. At a minimum, this delays when the Fed will act and how aggressively it acts. Furthermore, the One Big Beautiful Bill Act adds support to long-term interest rates. If this materializes, a significant recovery in construction activity could be delayed until the second half of 2026 – perhaps later.

About The Sullivan Report

The Sullivan Report delivers subscription-based economic forecasts and market updates tailored to the cement, concrete, construction, and aggregates industries. Its flagship publication, the Cement Outlook, is released three times a year and features 5-year forecast projections, expert analysis, and actionable insights to support informed decision-making and long-term strategic planning amid an evolving economic landscape.

Guided by renowned economist Ed Sullivan, The Sullivan Report also offers keynote presentations and customized forecasting services for organizations and regions seeking deeper, data-driven market intelligence. For more information, message us here, visit TheSullivanReport.com, or email us at info@thesullivanreport.com.